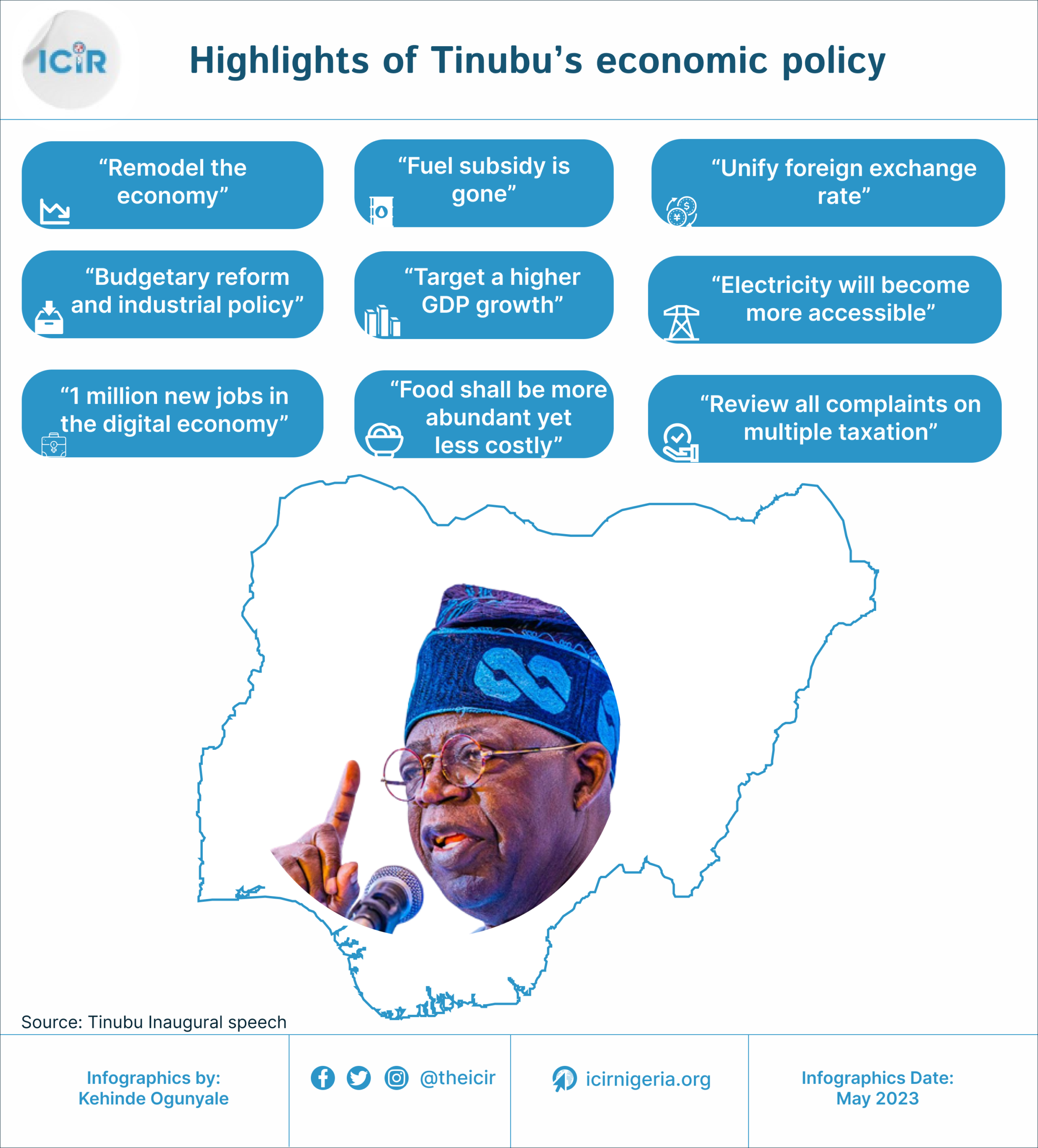

The administration of President Bola Tinubu will be two years old on May 29, 2025. He didn’t leave anyone in doubt as to the clear focus of his economic agenda from day one. At the inauguration ground in Eagle Square, Abuja, he made the now famous and impactful statement that “fuel subsidy is gone.” Fuel subsidy had been a monster that successive governments were afraid to tackle, perhaps for fear of its political ramifications, especially the reaction of the organised labour.

President Tinubu made it abundantly clear that tough decisions had to be made to prevent the collapse of the nation’s economy. The removal of fuel subsidy brought inflationary consequences, resulting in the increase in the prices of virtually all goods and services. To mitigate the negative impact, the president engineered the distribution of palliatives to the most vulnerable in society to cushion the negative effects of the end of the subsidy regime which lasted many decades.

President Tinubu also made another major economic decision to float the naira or merge the exchange rates (official and parallel markets) in order for the national currency to find its real value. On every occasion, he explained that what Nigerians were experiencing was temporary, and that, with time, they will enjoy the positive impact of his economic reforms. In less than two years, Nigerians have begun experiencing the positive impact of the reforms.

The International Monetary Fund (IMF) recently confirmed that Nigeria has fully repaid the $3.4billion financial support it received under the Rapid Financing Instrument (RFI) to cushion the economic impacts of the COVID-19 pandemic. The IMF’s Resident Representative for Nigeria, Mr Christian Ebeke said the repayment was completed on April 30, 2025. He clarified that Nigeria would however continue to make annual payments of approximately $30million in SDR-related charges over the next few years. This is good news for Nigeria because the repayment would boost the country’s international credit rating and strengthen the naira.

Nigeria’s overall Debt Stock, both external and domestic, of the Federal Government, the 36 states and the FCT, went down from $108.2billion dollars to $94billion dollars as of December 31, 2024.

The administration of President Tinubu has also cleared all the verified foreign exchange backlog of about $7billion, which made some foreign airlines to threaten to exit the country.